")

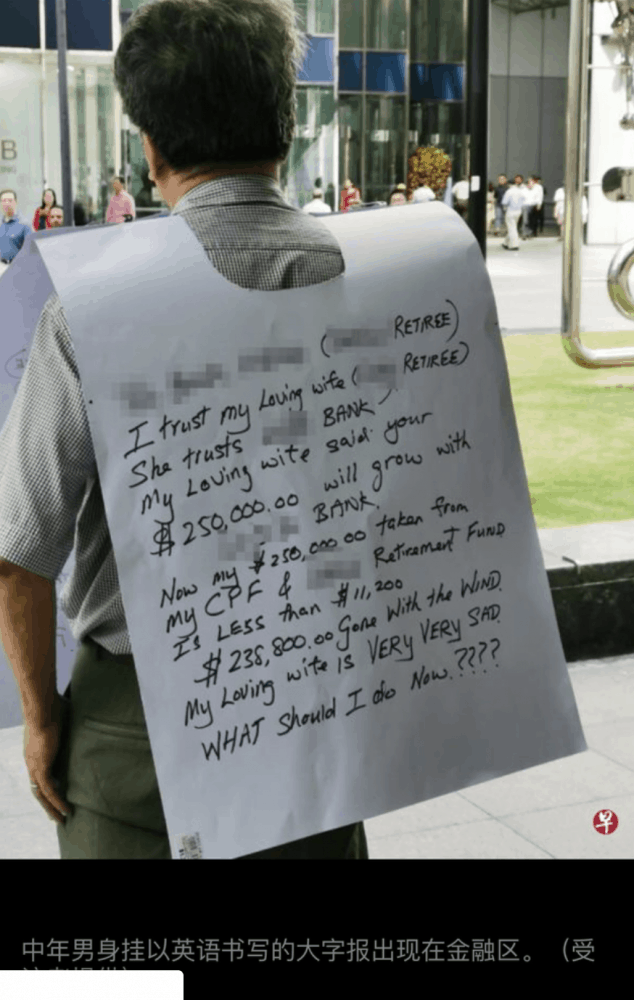

Earlier this year, a picture on the online forum Reddit of an elderly man who had lost a significant portion of his CPF savings after investing with a bank caused an online uproar.

The elderly Singaporean man had allegedly invested $250,000 worth of CPF savings with a bank as suggested by his wife. However, his investments incurred a loss of $238,000 leaving him with just $11,200 in CPF funds.

Since the post went viral, Singaporeans have been actively debating whether or not investing one’s CPF savings is a financially sound decision. Before we dive into that argument, we’re going lay down some key facts about the CPF Investment Scheme.

What Is The CPFIS?

The CPFIS refers to the Central Provident Fund Investment Scheme. The scheme allows CPF members to invest their Ordinary Account savings and Special Account savings into a range of investments.

Who Is Eligible For The CPFIS?

CPF members who wish to invest under the CPFIS must be at least 18 years old, not an undischarged bankrupt and have more than $20,000 in their Ordinary Account and/or $40,000 in their Special Account.

CPF members should also take note that they may only invest their OA savings up to 35% and 10% of their investible savings (the sum of one’s OA balance and the total amount of CPF withdrawn for investment and education).

Factors To Consider

There are several factors you ought to consider before investing your CPF savings in investments. Firstly, CPF members should consider the brokerage charges they will incur when making investments. Every transaction, including the purchase of Singapore Savings Bond incurs bank charges. Additionally, there are also annual expenses that apply to investments such as Unit Trusts and gold.

CPF members who wish to invest their savings into investments should be cautious and do so only after considering three key factors —risk tolerance, time horizon and financial position.

Risk tolerance refers to CPF member’s threshold when it comes to risk-taking. How much are they willing to lose to inevitable investment risks? Don’t forget to factor in brokerage or agent charges that apply whether or not returns or losses are made.

Time horizon involves the duration of one’s investments. How long does the investment last? How long can it continue to yield returns? Ultimately, the very purpose of having funds in your Ordinary Account and Special Account is to prepare financially for retirement. With this in mind, it may not be appropriate to invest funds that are meant to serve long-term needs.

The third factor that should be considered carefully would be your personal financial position. Think about your current and future financial commitments, and whether or not investing your retirement funds are a sound decision. If you foresee yourself depending quite heavily on CPF payouts to sustain yourself and your dependents post-retirement, investing your CPF savings may not be the best option for you.

“Should I invest my CPF savings under the CPFIS?”

As of 1 October 2018, the CPF board has made the CPFIS Self-Awareness Questionnaire mandatory for CPF members who wish to invest their savings in investments. The purpose mandating the Self-Awareness Questionnaire is to educate CPF members about investment products, information and concepts through online learning modules before they take the SAQ.

Results of the SAQ will help determine whether an individual is suitable for the CPFIS. Though this may seem like quite a tedious process, it is a good way to ensure that you are well-equipped with the relevant information. With a clearer picture of how investments under the CPFIS work, you are more likely to arrive at a logical and financially sound decision.

“What if I’m still unsure?”

CPF members who are still hesitant about investing their CPF savings under the CPFIS can take advantage of the estimation tools provided on the CPF website.

For example, CPF members who are intending to invest in Unit Trusts can use the Unit Trust Profit and Loss Calculator to estimate the profit or loss on their unit trust investments under the CPFIS.

Making Wise Financial Decisions

Investments may indeed appear very lucrative – using your CPF savings to invest may seem like it is an attractive and viable option since you do not have to fork out extra funds to make investments.

However, before you make your decision, do keep in mind that the interest rates of CPF funds are already very attractive. CPF members earn an interest rate of 2.5% p.a. for CPFOA (Ordinary Account) and 4% for CPFSA (Special Account), for just leaving their funds untouched.

The choice of not investing your CPF savings may be a wiser choice in the long run. If one uses CPF savings for investments, they are putting a good portion of their retirement funds on the line. That money has lots of potential to grow over the years, especially with the attractive interest rates offered by CPF.

Ultimately, CPF members must be sufficiently equipped with the right and relevant information and should have some degree of financial literacy before rushing into a decision. Before using CPF savings for investment, CPF members should also consider their personal financial position and whether or not it is safer to leave their funds untouched, in consideration of their long-term needs.

{kind=link}